|

|

Each Office Independently Owned & Operated

Posted by: Patrick Lofto

|

|

Posted by: Patrick Lofto

The national average house price is expected to increase by 9.1 per cent — to $620,400 — in 2021, the Canadian Real Estate Association (CREA) said today.

Shortages of supply, particularly in Ontario and Quebec, are expected to result in strong price growth, while Alberta and Saskatchewan are anticipated to see average prices pick up following several years of depreciation, the group said.

“Current trends and the outlook for housing market fundamentals suggest activity will remain relatively healthy through 2021, with prices either continuing to climb or remaining steady in all regions,” CREA said in a news release.

Posted by: Patrick Lofto

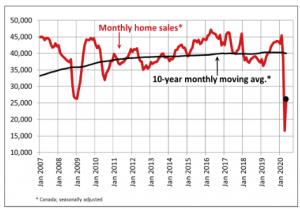

| Today’s release of July housing data by the Canadian Real Estate Association (CREA) showed a blockbuster July with both sales and new listings hitting their highest levels in 40 years of data. This continues the rebound in housing that began three months ago.

National home sales rose 26% month-over-month (m-o-m) in July, which translates to a 30.5% gain from a year ago (see chart below). July’s sales activity was the strongest for any month in history. According to Shaun Cathcart, CREA’s Senior Economist, “A big part of what we’re seeing right now is the snapback in activity that would have otherwise happened earlier this year. Recall that before the lockdowns, we were heading into the tightest spring market in almost 20 years. Things may have gone quiet for a few months, but ultimately the market we’re seeing right now is mostly the same one we were heading into back in March. That said, there are some new factors at play as well. There are listings that will come to the market because of COVID-19, but many properties are also not being listed right now due to the virus, as evidenced by inventories that are currently at a 16-year low. Some purchases will no doubt be delayed, but the new-found importance of home, lack of a daily commute for many, a desire for more outdoor and personal space, room for a home office, etc. will certainly also spur activity that otherwise would not have happened in a non-COVID-19 world.” For the third month in a row, transactions were up on a month-over-month basis across the country. Among Canada’s largest markets, sales rose by 49.5% in the Greater Toronto Area (GTA), 43.9% in Greater Vancouver, 39.1% in Montreal, 36.6% in the Fraser Valley, 31.8% in Hamilton-Burlington, 28.7% in Ottawa, 16.9% in London and St. Thomas, 15.7% in Calgary, 12.1% in Winnipeg, 9.7% in Edmonton and 5.4% in Quebec City. |

Posted by: Patrick Lofto

There was good news today on the housing front. Home sales surged by a record 56.9% in May from April’s unprecedented collapse. Data released this morning from the Canadian Real Estate Association (CREA) showed national home sales recovered roughly one-third of the COVID-induced loss between February and April (see chart below). On a year-over-year (y-o-y) basis, sales activity was still down almost 40%, but the jump in sales and an even larger surge in new listings shows pent-up demand remains for housing as buyers wish to take advantage of historically low mortgage rates.

Transactions were up on a month-over-month (m-o-m) basis across the country. Among Canada’s largest markets, sales rose by 53% in the Greater Toronto Area (GTA), and 69.4% in Hamilton-Burlington.

Despite the pandemic, home prices in the Greater Golden Horsehoe area around and including Toronto have fallen very little and remain well above year-ago levels. In Ottawa, Montreal and Moncton, prices have continued to climb, albeit at a slower pace than before.

Posted by: Patrick Lofto

Once again, the Canadian Mortgage and Housing Corporation (CMHC) is tightening the criteria to get a mortgage with less than a 20% down payment. Any potential home buyer with less than a 20% down payment must purchase default insurance on their loan and have a minimum down payment of 5%. CMHC is a federal Crown Corporation that provides such default insurance. Its mandate is to help Canadians access affordable housing options. Providing mortgage insurance to home buyers is one of its main activities. Mortgage default insurance protects lenders in the event a borrower ever stopped making payments and defaulted on their mortgage loan–a very infrequent occurrence in Canada.

There are private providers of default insurance as well–Genworth Financial Canada and Canada Guaranty. CMHC is the only insurer of mortgages for multi-unit residential properties, including large rental buildings, student housing and nursing and retirement homes. It is the largest provider of mortgage default insurance by far and is also the primary insurer for housing in small and rural communities.

Investment properties are not eligible for mortgage insurance. Because of this, the buyer needs at least a 20% down payment to buy an investment property. Homes costing more than $1 million, as well, are not eligible for mortgage insurance. Typically, the lender chooses the mortgage insurer.